So, your loved one has finally found their dream apartment and is getting ready to sign the lease. The only problem? The landlord or property manager requires them to find an apartment guarantor that would sign the lease with them.

With the limited availability in the housing market, you probably want to help them secure the apartment and are ready to vouch for them.

But before you do, it’s important to understand the obligations that come with being a guarantor, as well as what you’ll need to actually become one. This article will walk you through everything you need to know.

An apartment guarantor—also often called a co-signer, which isn’t entirely correct—is a person or a third-party entity that takes on the legal responsibility of paying the rent if the tenant is unable to do so.

Landlords and property managers sometimes require potential tenants to have guarantors because this adds another layer of security and insurance. If the tenant fails to pay their rent, they can always collect the outstanding amount from the guarantor.

(Guarantors are called guarantors because they guarantee that the agreed-upon money sum will be paid to the landlord or property manager.)

In order to become an apartment guarantor, you’ll have to sign the lease agreement alongside the tenant, as well as meet some other requirements that we’ll discuss below.

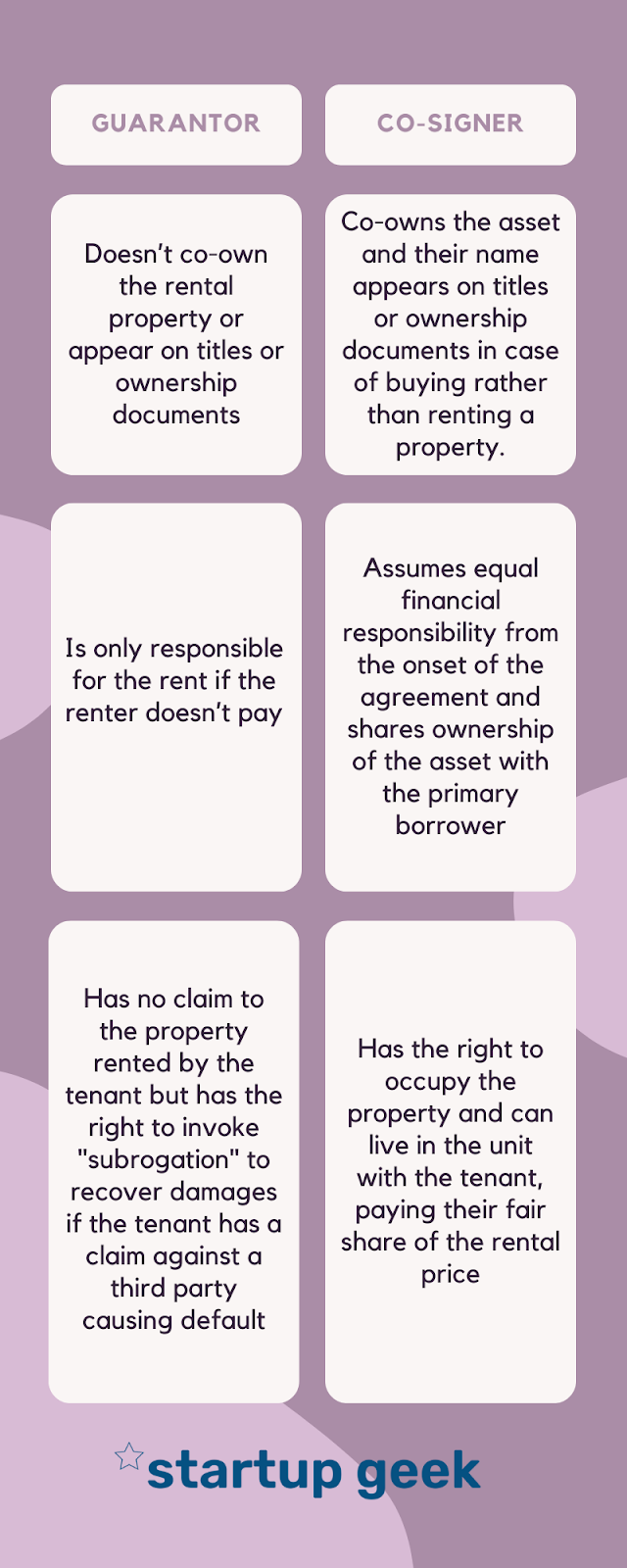

As mentioned, the terms “guarantor” and “co-signer” are often used interchangeably. However, the two have distinct differences when it comes to their roles and responsibilities.

Here’s a quick breakdown of the key differences between a guarantor and a co-signer.

A guarantor:

A co-signer, on the other hand:

So, while both guarantors and co-signers provide financial support in rental agreements, guarantors do not have the right to occupy it.

Co-signers, however, can live in the property alongside the primary borrower. In the case of apartment purchases, they also co-own the asset alongside the primary buyer.

Essentially, co-signers have more financial obligations but also get more in return than guarantors.

Tenants don’t always need guarantors to get their rental application approved. However, this is the most likely scenario for:

The specific circumstances and the necessity of a guarantor will depend on the specific landlord’s or property manager’s requirements.

Generally, any person that is financially stable and has a good credit history can be a guarantor.

However, the guarantors are usually expected to meet some more specific requirements. These may include:

As mentioned, the specific requirements for a guarantor can vary depending on the property manager or landlord, so it’s essential to clarify their expectations before proceeding.

Usually, tenants choose people they have personal connections with to be their guarantors—such as a family member, close friend, or even a business associate. For example, students often turn to parents or guardians for this purpose.

However, tenants can also choose third-party organizations, i.e., specialized companies offering guarantor services, as their guarantors.

Such companies are often more educated about what the role of a guarantor entails and have a better understanding of the essential details that need to be outlined in the agreement. This ensures that all necessary information is included, and both parties are protected from any potential exploitation.

Some individuals may not be eligible or suitable for the role of a guarantor. This includes persons who do not meet the minimum age requirement, which is usually 18 or 21 depending on where you live.

Additionally, landlords may also reject individuals with poor credit history or unstable job situations due to concerns about their ability to fulfill the financial obligations that come with being a guarantor.

Landlords rely on the guarantor’s financial stability and responsible track record to ensure that rent payments will be made in a timely manner, and rejecting individuals with poor credit or unstable job situations helps mitigate the risk of potential default or payment issues.

These are the most common reasons for someone to be rejected or unsuitable for a guarantor, but there may be others depending on each landlord’s specific criteria.

So, how do you actually become an apartment guarantor? We’ll walk you through the five essential steps.

First things first: you need to understand the financial obligations that come with being a guarantor and ensure you have the means to meet them.

To do so, ask yourself the following questions:

These questions aren’t meant to scare you but to give you a more realistic perspective of what it means to be a guarantor. Answering them will help you assess whether you’re truly suitable for the role at the moment.

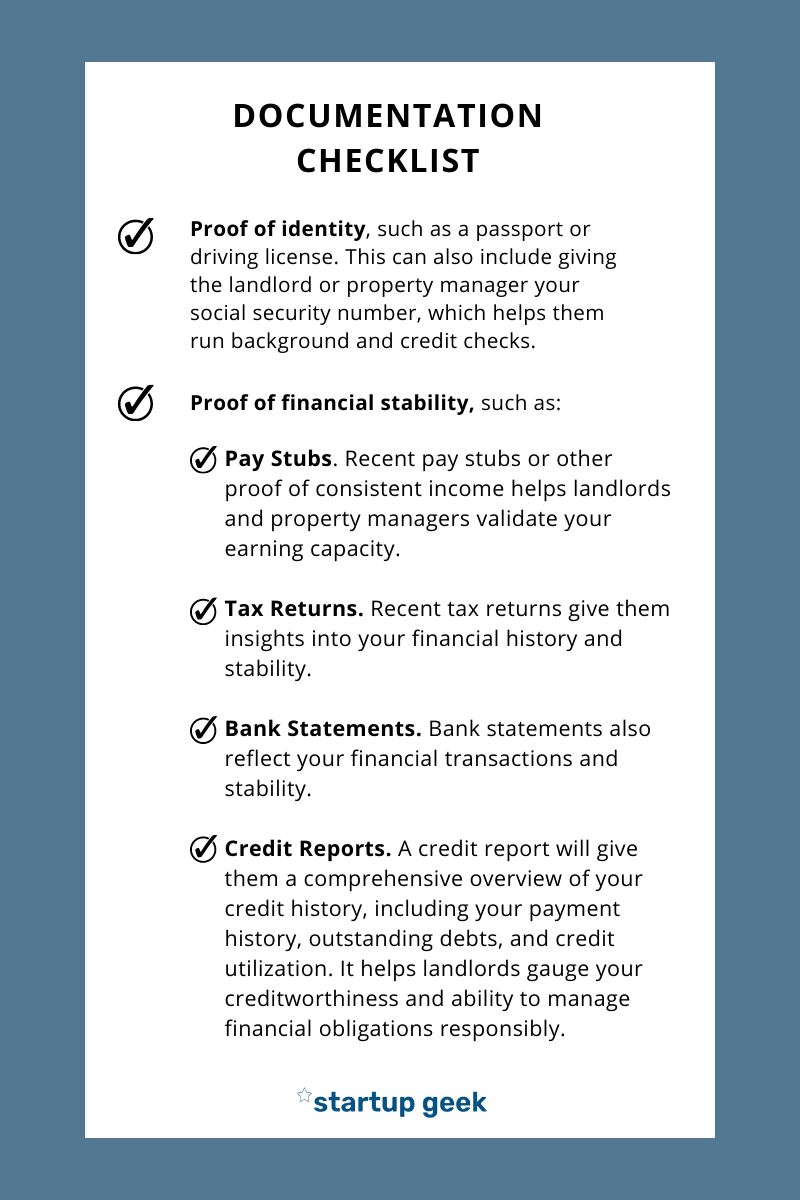

Landlords and property management firms need a way to screen and verify guarantors. In order to do so, they’ll typically require two types of documents:

When it comes to proving financial stability, the landlord or property manager may ask you to submit one or several of the following documents:

Some landlords and property managers may also ask for additional proof, such as your personal references. While some landlords may feel that personal references have little value – since applicants provide the names of individuals who’ll give a good reference – others (while acknowledging the potential for bias), treat personal references as third-party opinions that they can use to compare patterns of behavior observed over time.

Being a guarantor for someone is a big decision, so you need to make sure there’s mutual trust between you and whoever you’re vouching for.

So, it’s crucial you have an open and transparent conversation with the applicant before you sign anything. Clarify expectations, responsibilities, and the terms of your agreement.

Discuss topics such as:

Clear communication will help establish a strong foundation and ensure that both of you are on the same page about your roles and obligations throughout the lease term.

Work closely with the landlord or property manager throughout the process to ensure compliance with their requirements.

As mentioned, they may request additional documentation or have specific procedures for becoming a guarantor, so it’s crucial that you can discuss them at any point.

Also, don’t be afraid to ask questions if you have them. This is crucial if you want to avoid getting yourself in a situation you don’t want to be in. Better to be safe than sorry!

Once all parties are satisfied with the terms and conditions, it’s time to sign the necessary documents as a guarantor. This means you’ll have to co-sign the lease agreement alongside the tenant and the landlord or property manager, but you may also be asked to sign some additional documents.

Carefully review the agreement and make sure you understand your legal obligations as a guarantor. Also, ensure you fully comprehend the potential consequences of default by the tenant, such as the impact on your credit history and the financial implications it may have for you.

Seek legal advice if needed to ensure you are fully informed about your rights and obligations.

Once you’ve considered all the steps needed to become a guarantor—and all the pros and cons—you may have decided that you’re not ready or willing to take on that role.

That’s perfectly fine. Being a guarantor is a big commitment.

In that case, you should communicate your decision honestly and respectfully to your loved one. While it may be a difficult conversation, it’s crucial you prioritize your own financial well-being and comfort level.

You can also recommend them suitable alternatives. One option is, for example, using a guarantor service.

Guarantor services provide the financial reassurance that landlords and property managers require. While using them comes with a fee, it may be a viable solution if an applicant doesn’t have a suitable personal candidate for the role.

The guarantor service fees are typically based on the applicant’s credit score or their annual rent.

Alternatively, the applicant could also try exploring additional options and communicating openly with landlords or property managers. Some may be willing to accept other forms of assurance, such as a higher security deposit or a few months’ rent in advance.

If even that fails, you can offer your loved one some assistance in their search for new apartments. Ultimately, it’s key that you and the applicant find the right solution that works for everyone.

In case you’re still indecisive about being a guarantor, let’s explore a few more questions you may have.

If a guarantor fails to fulfill their obligations, the landlord or property manager may take legal action against them to recover the unpaid rent or damages. The guarantor’s credit score may also be negatively affected, making it more difficult for them to secure loans or other financial arrangements in the future.

Yes, a guarantor can live at the same address as the tenant but they are not entitled to that by simply being a guarantor.

No, a guarantor does not have ownership rights to the property being rented or leased. Their role is solely to provide financial reassurance to the landlord or property manager by guaranteeing rent payments.

The tenant remains the sole occupant and has the rights and responsibilities associated with tenancy.

Yes, a guarantor can be retired, since the primary concern for landlords or property managers is the guarantor’s financial stability and ability to fulfill their obligations.

As long as a retired individual meets the financial criteria and has a reliable income source, they can serve as a guarantor. In that case, landlords and property managers may request proof of retirement income or other financial documentation.

Being a guarantor is a big commitment, and you shouldn’t consider taking it on for just anyone—including your family members or friends if you know them to be unreliable.

However, if there is mutual trust between you and the applicant, and you’re ready to vouch for them, then there’s nothing stopping you. This blog post gives you all the information you need to become a guarantor, and all that’s left to do is discuss the specificities with the landlord or property manager.

Remember: if you need more clarity about your agreement, don’t hesitate to ask questions or seek legal advice. Your peace of mind and financial well-being should be a top priority.

Credit: Written by Oran Yehiel, Founder at StartupGeek.com